Prediction Housing Prices in Iowa. Exploratory Data Analysis, Dealing with Missing Values, Data Munging, Ensembled Regression Model using Stacked Regressor, XGBoost and microsoft LightGBM

Currently in top 5% (143rd in 1890 participants), Last ran on: July 1st, 2017

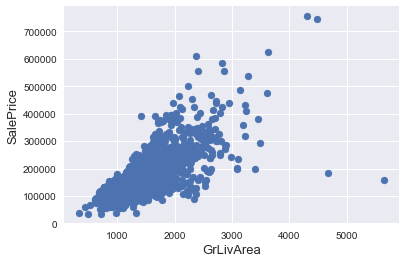

Documentation for the Ames Housing Data indicates that there are outliers present in the training data 1: http://ww2.amstat.org/publications/jse/v19n3/Decock/DataDocumentation.txt

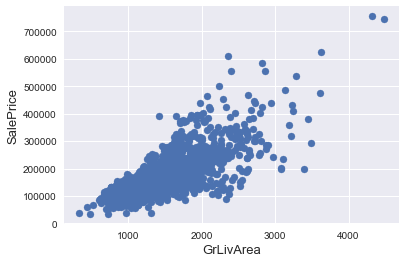

We can see at the bottom right two with extremely large GrLivArea that are of a low price. These values are huge oultliers. Therefore, we can safely delete them.

Note :

Outliers removal is not always safe. We decided to delete these two as they are very huge and really bad ( extremely large areas for very low prices).

There are probably others outliers in the training data. However, removing all them may affect badly our models if ever there were also outliers in the test data. That’s why , instead of removing them all, we will just manage to make some of our models robust on them. You can refer to the modelling part of this notebook for that.

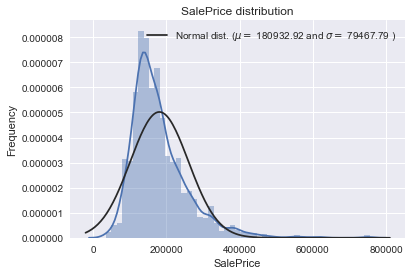

Target Variable

SalePrice is the variable we need to predict. So let’s do some analysis on this variable first.

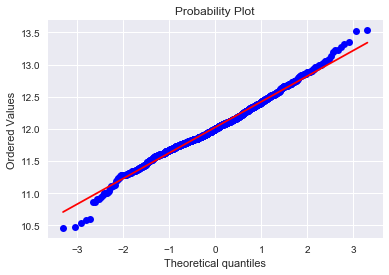

The target variable is right skewed. As (linear) models love normally distributed data , we need to transform this variable and make it more normally distributed.

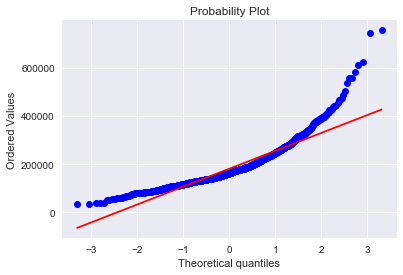

Log-transformation of the target variable

The skew seems now corrected and the data appears more normally distributed.

Features engineering

let’s first concatenate the train and test data in the same dataframe

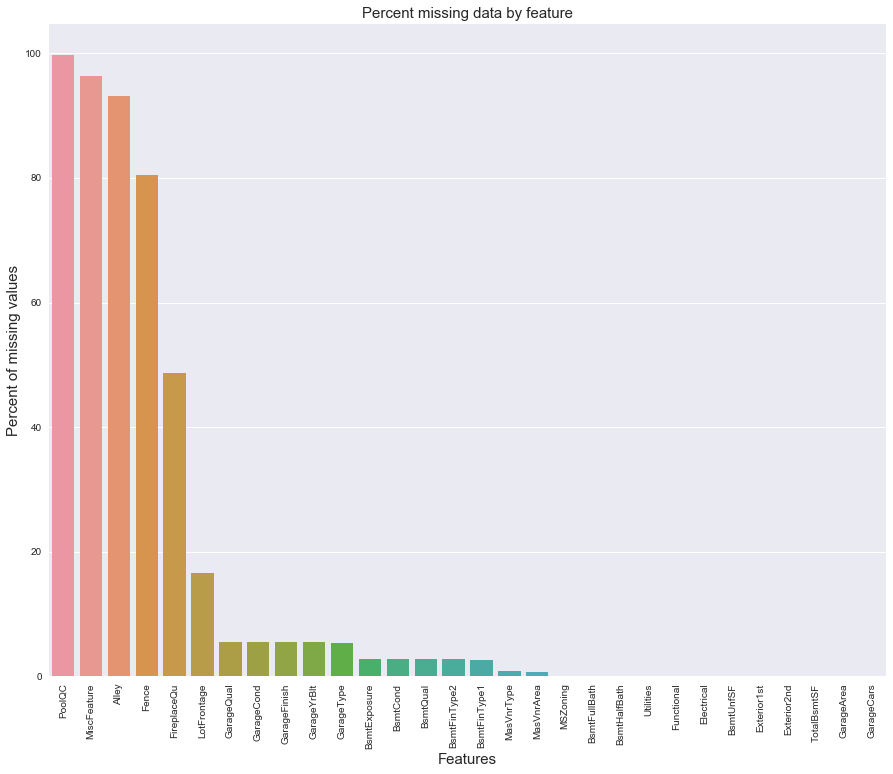

Missing Data

Missing Ratio

PoolQC

99.691

MiscFeature

96.400

Alley

93.212

Fence

80.425

FireplaceQu

48.680

LotFrontage

16.661

GarageQual

5.451

GarageCond

5.451

GarageFinish

5.451

GarageYrBlt

5.451

GarageType

5.382

BsmtExposure

2.811

BsmtCond

2.811

BsmtQual

2.777

BsmtFinType2

2.743

BsmtFinType1

2.708

MasVnrType

0.823

MasVnrArea

0.788

MSZoning

0.137

BsmtFullBath

0.069

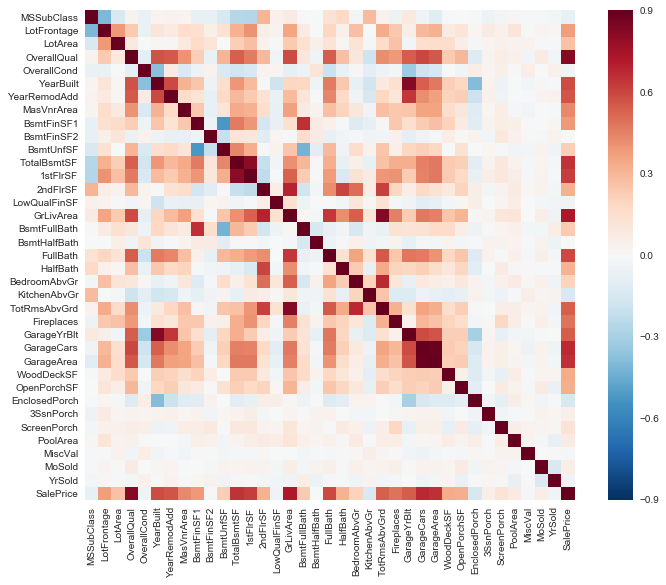

Data Correlation

Imputing missing values

We impute them by proceeding sequentially through features with missing values

PoolQC : data description says NA means “No Pool”. That make sense, given the huge ratio of missing value (+99%) and majority of houses have no Pool at all in general.

LotFrontage : Since the area of each street connected to the house property most likely have a similar area to other houses in its neighborhood , we can fill in missing values by the median LotFrontage of the neighborhood.

#Group by neighborhood and fill in missing value by the median LotFrontage of all the neighborhoodall_data["LotFrontage"]=all_data.groupby("Neighborhood")["LotFrontage"].transform(lambdax:x.fillna(x.median()))

GarageType, GarageFinish, GarageQual and GarageCond : Replacing missing data with None

BsmtQual, BsmtCond, BsmtExposure, BsmtFinType1 and BsmtFinType2 : For all these categorical basement-related features, NaN means that there is no basement.

Utilities : For this categorical feature all records are “AllPub”, except for one “NoSeWa” and 2 NA . Since the house with ‘NoSewa’ is in the training set, this feature won’t help in predictive modelling. We can then safely remove it.

all_data=all_data.drop(['Utilities'],axis=1)

Functional : data description says NA means typical

Transforming some numerical variables that are really categorical

Label Encoding some categorical variables that may contain information in their ordering set

Adding one more important feature

Since area related features are very important to determine house prices, we add one more feature which is the total area of basement, first and second floor areas of each house

Skewed features

Skew

MiscVal

21.940

PoolArea

17.689

LotArea

13.109

LowQualFinSF

12.085

3SsnPorch

11.372

LandSlope

4.973

KitchenAbvGr

4.301

BsmtFinSF2

4.145

EnclosedPorch

4.002

ScreenPorch

3.945

Box Cox Transformation of (highly) skewed features

We use the scipy function boxcox1p which computes the Box-Cox transformation of \(1 + x\).

Note that setting \( \lambda = 0 \) is equivalent to log1p used above for the target variable.

See this page for more details on Box Cox Transformation as well as [the scipy function’s page]2: http://onlinestatbook.com/2/transformations/box-cox.html [2]: https://docs.scipy.org/doc/scipy-0.19.0/reference/generated/scipy.special.boxcox1p.html

There are 59 skewed numerical features to Box Cox transform

Modelling

In this approach, we add a meta-model on averaged base models and use the out-of-folds predictions of these base models to train our meta-model.

The procedure, for the training part, may be described as follows:

Split the total training set into two disjoint sets (here train and .holdout )

Train several base models on the first part (train)

Test these base models on the second part (holdout)

Use the predictions from 3) (called out-of-folds predictions) as the inputs, and the correct responses (target variable) as the outputs to train a higher level learner called meta-model.

The first three steps are done iteratively . If we take for example a 5-fold stacking , we first split the training data into 5 folds. Then we will do 5 iterations. In each iteration, we train every base model on 4 folds and predict on the remaining fold (holdout fold).

So, we will be sure, after 5 iterations , that the entire data is used to get out-of-folds predictions that we will then use as new feature to train our meta-model in the step 4.

For the prediction part , We average the predictions of all base models on the test data and used them as meta-features on which, the final prediction is done with the meta-model.

On this gif, the base models are algorithms 0, 1, 2 and the meta-model is algorithm 3. The entire training dataset is A+B (target variable y known) that we can split into train part (A) and holdout part (B). And the test dataset is C.

B1 (which is the prediction from the holdout part) is the new feature used to train the meta-model 3 and C1 (which is the prediction from the test dataset) is the meta-feature on which the final prediction is done.

Define a cross validation strategy

We use the cross_val_score function of Sklearn. However this function has not a shuffle attribut, we add then one line of code, in order to shuffle the dataset prior to cross-validation

Base models

LASSO Regression :

This model may be very sensitive to outliers. So we need to made it more robust on them. For that we use the sklearn’s Robustscaler() method on pipeline

Simplest Stacking approach : Averaging base models

We begin with this simple approach of averaging base models. We build a new class to extend scikit-learn with our model and also to laverage encapsulation and code reuse (inheritance)

Averaged base models class

classAveragingModels(BaseEstimator,RegressorMixin,TransformerMixin):def__init__(self,models):self.models=models# we define clones of the original models to fit the data indeffit(self,X,y):self.models_=[clone(x)forxinself.models]# Train cloned base modelsformodelinself.models_:model.fit(X,y)returnself#Now we do the predictions for cloned models and average themdefpredict(self,X):predictions=np.column_stack([model.predict(X)formodelinself.models_])returnnp.mean(predictions,axis=1)

Averaged base models score

We just average four models here ENet, GBoost, KRR and lasso. Of course we could easily add more models in the mix.

averaged_models=AveragingModels(models=(ENet,GBoost,KRR,lasso))score=rmsle_cv(averaged_models)print(" Averaged base models score: {:.4f} ({:.4f})\n".format(score.mean(),score.std()))

class="highlight">

1

Averaged base models score: 0.1091 (0.0075)

Wow ! It seems even the simplest stacking approach really improve the score . This encourages us to go further and explore a less simple stacking approch.

Less simple Stacking : Adding a Meta-model

Stacking averaged Models Class

classStackingAveragedModels(BaseEstimator,RegressorMixin,TransformerMixin):def__init__(self,base_models,meta_model,n_folds=5):self.base_models=base_modelsself.meta_model=meta_modelself.n_folds=n_folds# We again fit the data on clones of the original modelsdeffit(self,X,y):self.base_models_=[list()forxinself.base_models]self.meta_model_=clone(self.meta_model)kfold=KFold(n_splits=self.n_folds,shuffle=True,random_state=156)# Train cloned base models then create out-of-fold predictions# that are needed to train the cloned meta-modelout_of_fold_predictions=np.zeros((X.shape[0],len(self.base_models)))fori,modelinenumerate(self.base_models):fortrain_index,holdout_indexinkfold.split(X,y):instance=clone(model)self.base_models_[i].append(instance)instance.fit(X[train_index],y[train_index])y_pred=instance.predict(X[holdout_index])out_of_fold_predictions[holdout_index,i]=y_pred# Now train the cloned meta-model using the out-of-fold predictions as new featureself.meta_model_.fit(out_of_fold_predictions,y)returnself#Do the predictions of all base models on the test data and use the averaged predictions as #meta-features for the final prediction which is done by the meta-modeldefpredict(self,X):meta_features=np.column_stack([np.column_stack([model.predict(X)formodelinbase_models]).mean(axis=1)forbase_modelsinself.base_models_])returnself.meta_model_.predict(meta_features)

Stacking Averaged models Score

To make the two approaches comparable (by using the same number of models) , we just average Enet KRR and Gboost, then we add lasso as meta-model.

'''RMSE on the entire Train data when averaging'''print('RMSLE score on train data:')print(rmsle(y_train,stacked_train_pred*0.70+xgb_train_pred*0.15+lgb_train_pred*0.15))